IRC §129

DCFSA Nondiscrimination Testing Calculator

The $7,500 cap changes the math on the 55% Average Benefits Test. Model your plan's NDT outcome and build a strategy to pass.

The $7,500 cap changes the math on the 55% Average Benefits Test. Model your plan's NDT outcome and build a strategy to pass.

5%+ owners are a subset of HCEs - they're already included in your HCE numbers above. These fields identify how many of your HCE participants are owners, so we can run the separate 25% concentration test.

| $5,000 cap (pre-2026) | $7,500 cap (2026) | |

|---|---|---|

| Avg. benefit - HCEs | $0 | $0 |

| Avg. benefit - Non-HCEs | $0 | $0 |

| Ratio | 0% | 0% |

| Result | - | - |

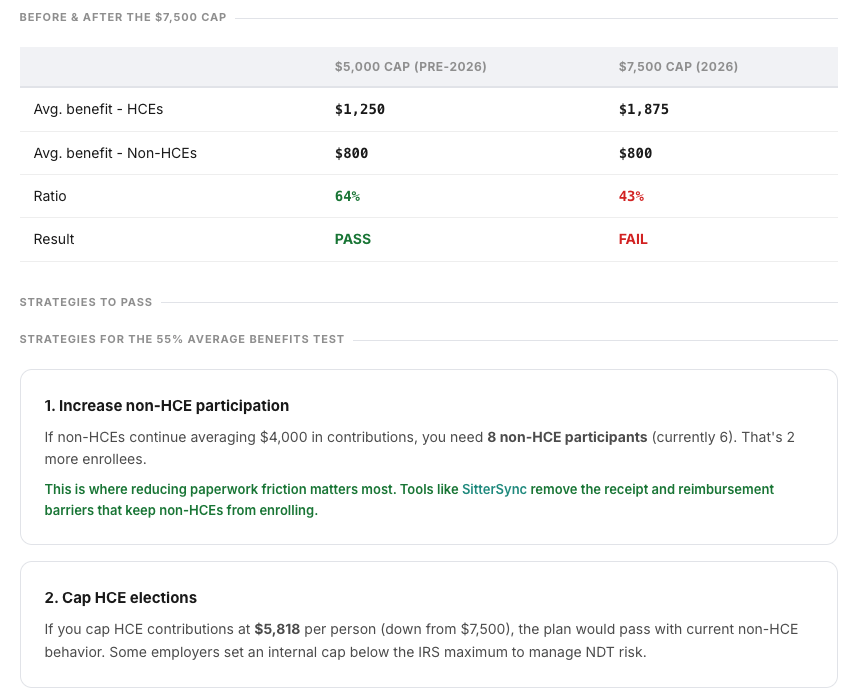

I was watching a webinar from EBC presented by Sarah Fowles on the OBBBA's impact on dependent care benefits, and she walked through a case study that stopped me cold: a plan that passed NDT comfortably under the old $5,000 cap was now failing under the new $7,500 cap - with no change in employee behavior. Just one HCE maxing out the new limit was enough to flip the result from 64% pass to 43% fail.

The math isn't complicated, but most benefits teams don't have a quick way to model it. They find out they've failed when the TPA runs the test after plan year-end - by which point it's too late to fix. HCE contributions get reclassified as taxable income, W-2s get corrected, and everyone has a bad day.

I built this calculator so employers can run the numbers before open enrollment, not after. Plug in your HCE/non-HCE counts and contribution patterns, see whether you pass or fail, and - if you fail - see exactly what it takes to get back to 55%. The strategies aren't theoretical. They're the same levers your TPA would recommend, just modeled in real time so you can plan ahead.

- Drew Chambers, Co-founder SitterSync

Under IRC §129, Dependent Care Assistance Programs (which includes DCFSA plans) must pass nondiscrimination testing to maintain their tax-advantaged status. The 55% Average Benefits Test is the primary test most plans use.

The test compares the average benefit provided to non-HCEs against the average benefit provided to HCEs. The non-HCE average must be at least 55% of the HCE average.

Why the $7,500 cap changes everything: Under the old $5,000 limit, HCE contributions were naturally capped. A single HCE maxing out created a modest average across the eligible HCE pool. With the new $7,500 limit, that same HCE's contribution is 50% higher - but non-HCE behavior typically doesn't change as fast. The denominator stays the same while the HCE numerator jumps, and plans that passed for years suddenly fail. Sarah Fowles' case study at EBC showed this exact scenario: same employer, same employees, same non-HCE contributions - just one HCE electing the new max was enough to flip the result.

The key detail that trips people up: the average benefit is calculated across all eligible employees in that group - not just participants. Every non-participating employee counts as $0 in the average. This is why participation rate matters so much.

This means a plan with 200 eligible non-HCEs but only 10 participants is dividing by 200, not 10. Low participation among non-HCEs is the most common reason plans fail - and it's the most fixable.

Who is an HCE? For 2026, a highly compensated employee is anyone who earned more than $155,000 in the prior year (2025) or is a more-than-5% owner at any time during the current or prior year. Owners are always HCEs by definition - they're tested as part of the HCE group in the 55% test AND separately in the 25% concentration test. Source: IRS definitions.

IRC §129(d)(4) adds a second, separate test: no more than 25% of total DCFSA benefits paid during the plan year can go to individuals who own more than 5% of the company. This includes shareholders, partners, and sole proprietors.

5%+ owners are already counted as HCEs in the 55% test above. The 25% concentration test is an additional check specifically on how much of the total plan goes to owners. A plan must pass both tests. This is especially relevant for smaller companies where an owner or a few partners participate in the DCFSA and their contributions make up a large share of total plan benefits.

Example: A company has $50,000 in total DCFSA contributions across all employees. If a 10% shareholder contributes $7,500 and another 8% partner contributes $7,500, that's $15,000 from 5%+ owners - 30% of total benefits. The plan fails the concentration test, and the owner benefits become taxable.

The $7,500 cap makes this harder too. Under the old $5,000 limit, two owners maxing out contributed $10,000. Under the new $7,500 limit, that same pair contributes $15,000 - a 50% increase that can push the owner share above 25% without any change in non-owner behavior.

If your DCFSA plan fails the 55% test, the excess benefits provided to HCEs become taxable income. The HCEs lose the pre-tax treatment on some or all of their contributions. If the 25% owners test fails, the benefits paid to 5%+ owners are reclassified as taxable. Either way, it means payroll adjustments, W-2 corrections, and a compliance headache nobody wants to deal with retroactively.

The better approach is to model it before open enrollment and act proactively. Plans typically have four levers:

Passing NDT means more FICA savings. Every non-HCE dollar contributed to the DCFSA saves the employer 7.65% in FICA taxes. Higher non-HCE participation doesn't just help you pass NDT - it directly reduces your payroll tax bill. Use the DCFSA ROI Calculator to model the employer savings from increased participation.